ArmInfo.S&P Global Ratings has revised Armenia outlook to positive on growth, potential improvement in regional security.

Overview

Ongoing efforts to normalize relations between Armenia and Azerbaijan could reduce the likelihood of future military escalation, easing regional security risks.

We project Armenia's economic growth will soften to a still high annual average of 5% in 2026-2029 as resilient domestic demand mitigates the gradual tapering off of capital and labor inflows from Russia.

Despite Armenia's still vulnerable balance of payments, its moderate net general government debt of 43% of GDP, a flexible exchange rate, and international reserves that have recently reached a high of $5.2 billion (18% of GDP) provide buffers against unanticipated shocks.

We revised our outlook on Armenia to positive from stable. At the same time, we affirmed our 'BB-/B' ratings. Rating Action

On Feb. 20, 2026, S&P Global Ratings revised its outlook on Armenia to positive from stable. Simultaneously, we affirmed our 'BB-/B' long- and short-term foreign and local currency sovereign credit ratings. Outlook

The revision of the outlook to positive reflects our view that there is the potential for improvement in regional geopolitical and security dynamics, specifically further progress toward normalizing diplomatic and trade relations between Armenia and Azerbaijan. We also view Armenia's growth prospects as favorable, while higher levels of the Central Bank of Armenia's (CBA's) international reserves and a flexible exchange rate should help mitigate possible unanticipated external shocks. Downside scenario

We could take a negative rating action should regional geopolitical risks escalate markedly or labor and capital inflows from Russia sharply reverse, weighing on Armenia's economic, fiscal, and balance-of-payments performance. Upside scenario

We could consider a positive rating action if security and geopolitical risks continue to recede durably. Upside potential could also arise if Armenia's fiscal outcomes significantly outperform our projections or if balance-of-payments vulnerabilities ease, supported by a further sustained increase in the CBA's international reserves. Rationale

Armenia's exposure to still-material, albeit moderating, geopolitical and external security risks, its evolving institutional settings, moderate per capita income levels, and balance-of-payments vulnerabilities constrain the ratings. The ratings are supported by Armenia's prudent policy frameworks, its strong growth outlook, moderating fiscal risks, and the improved foreign exchange reserve position.

Institutional and economic profile: Progress in normalizing relations with Azerbaijan, volatile ties with Russia, and elevated domestic political uncertainty

Progress in negotiations with Azerbaijan could reduce near-term security risks, although the prospect of a durable peace agreement still depends on signing a binding agreement and its effective implementation.

Political relations with Russia remain volatile, while Armenia's dependence on trade and financial flows from Russia remains high.

We expect macroeconomic policy continuity after the upcoming parliamentary elections in June 2026, yet the domestic political landscape remains fragmented.

Peace negotiations between Armenia and Azerbaijan have progressed, reducing the probability of further military escalation in the near term, in our view. Azerbaijan consolidated its control over Nagorno-Karabakh through a military offensive in late 2023, following a 44-day war in 2020. With Nagorno-Karabakh no longer contested, negotiations between the two countries have focused on a comprehensive peace framework centered on mutual recognition of sovereignty and territorial integrity, border delimitation, and the establishment of diplomatic relations. The August 2025 U.S.-brokered agreement marked an important political milestone, signaling commitment at the leadership level and helping to stabilize the security environment. Initial normalization steps have led to modest improvements in regional connectivity and trade, alongside an ongoing Armenia- Turkiye normalization process aimed at reopening borders and establishing diplomatic relations.

However, the path to signing and ratifying the peace agreement between Armenia and Azerbaijan remains complex and will take time, in our view. The durability of the agreement will depend on both sides' willingness to implement politically sensitive decisions, the credibility of enforcement, and security arrangements. Outstanding issues include the sequencing and enforcement of border delimitation and the absence of clearly defined security guarantees. It also remains unclear, in our view, to what extent Russia will remain supportive of an international diplomatic effort to normalize Armenia- Azerbaijan relations that so far has been made without its direct participation.

Domestic political constraints in Armenia may also add a layer of uncertainty to peace agreement negotiations. The authorities are preparing a new constitution, with the draft expected by March and a referendum planned for after the June parliamentary elections. Yet it remains unclear whether the preamble will retain references to the 1990 Declaration of Independence, a key point disputed with Azerbaijan, given the latter views such references as implying territorial claims. Meanwhile, already high domestic political polarization has been further amplified by tensions between the government and the Armenian Apostolic Church, which enjoys some public support. Since 2024, part of the senior clergy has become closely involved in opposition protests against the government's border and foreign policy decisions. The dispute escalated further in 2025, when authorities arrested several church-linked figures, accusing them of attempts to seize power. Against this background, upcoming constitutional changes and sensitive foreign policy negotiations could face headwinds, in our view.

Relations between Armenia and Russia have deteriorated since 2023, marking a shift away from Armenia's longstanding reliance on Moscow as its primary security anchor. The relationship weakened sharply after Russia failed to intervene during Azerbaijan's 2023 military operation in Nagorno-Karabakh, prompting Yerevan to publicly question the value of Russian security guarantees and to freeze participation in Russia-led regional security structures.

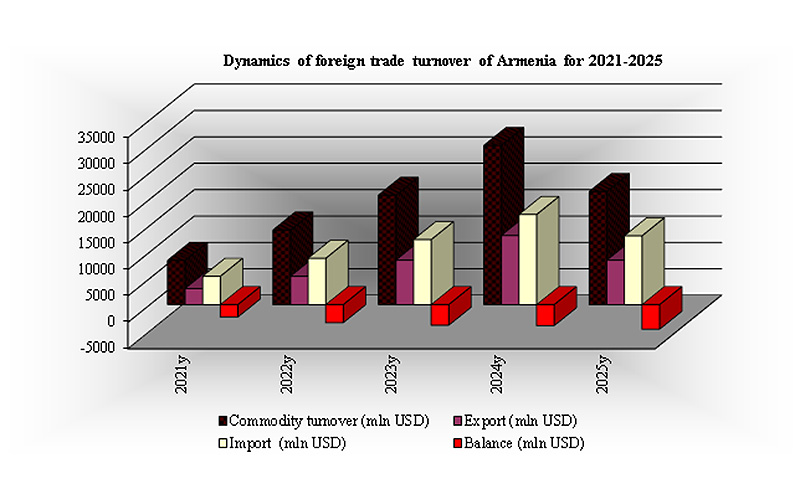

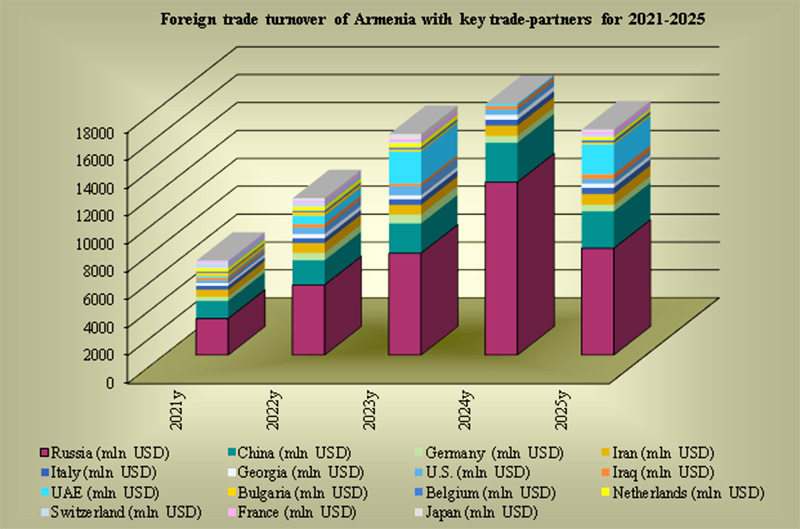

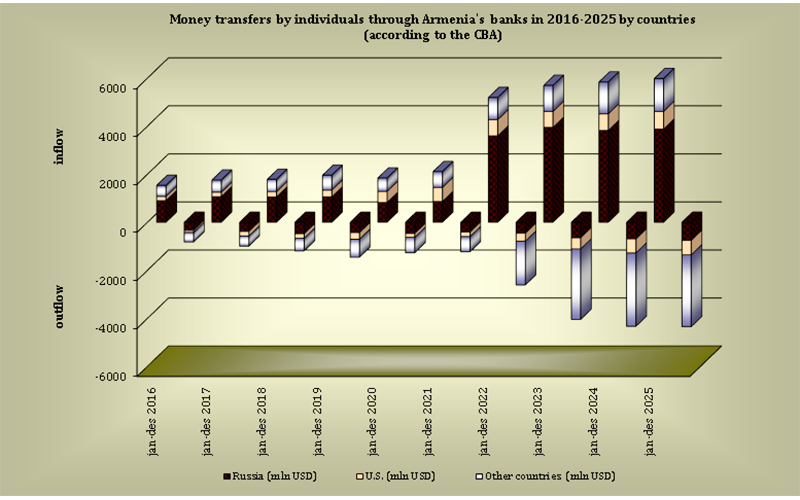

Armenia has increasingly pursued a more diversified foreign and security policy, but its economic links with Russia remain high. Armenia has deepened engagement with Western partners, hosted EU monitoring missions, and signaled greater alignment with international legal frameworks, although economic and financial exposure to Russia is still substantial. Russia continues to account for over 36% of Armenia's total exports, a third of imports, half of financial inflows (including labor remittances), and 60% of the country's total energy needs. These links have actually increased in the aftermath of Russia's invasion of Ukraine, when Armenia emerged as one of the key destinations for Russian individuals and businesses trying to escape domestic political risks and the adverse effects of international sanctions. We consider that Armenia's ability to balance political distancing from Russia with continued significant economic ties will be important for its medium-term economic prospects, given that Armenia remains exposed to potential adverse shifts in Russia's policies.

Armenia's upcoming parliamentary elections scheduled for June represent an important near-term test for political stability and policy continuity. Recent opinion polls signal that Prime Minister Nikol Pashinyan and his Civil Contract party continue to lead the field, albeit with lower approval levels than in the aftermath of the 2021 snap elections. At the same time, the opposition remains highly fragmented, spanning former government-linked figures, nationalist groups, protest movements, and church-aligned actors, none of which has yet coalesced around a single leader with broad national appeal or clear electoral momentum. Our base-line expectation is for broad political continuity after the June elections, with the new government continuing to focus on reaching a full peace agreement with Azerbaijan and not reversing related previous commitments for populist reasons.

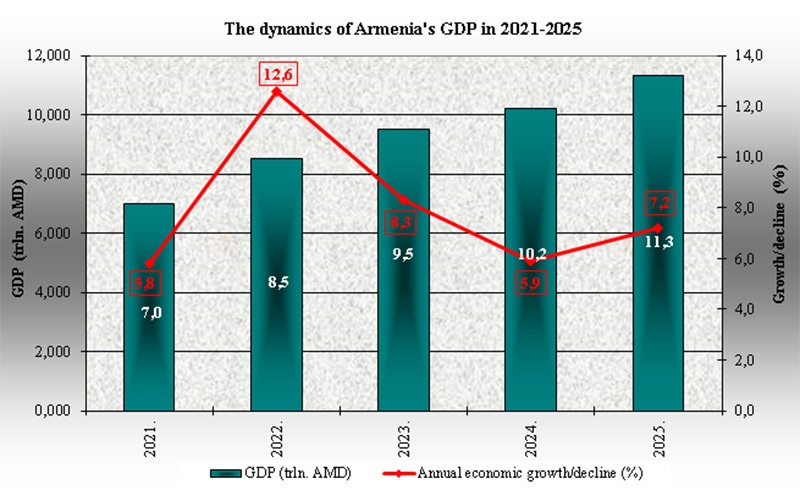

We forecast Armenia's real GDP will expand by 5.3% this year and 4.8% in 2027. Armenia's growth averaged a high 7.8% in 2022-2025; one of the fastest growth rates among the 143 sovereigns we rate. Softer growth in the medium term reflects our expectations that growth drivers linked to the Russia-related re-exports activity and labor and capital inflows will continue to moderate. We expect growth to remain primarily consumption- and private-investment-driven, supported by resilient labor market conditions, improving real incomes amid moderating inflation, and supportive credit conditions, alongside continued investment in construction and services.

Flexibility and performance profile: Fiscal consolidation is progressing, but balance-of-payments vulnerabilities remain

Fiscal consolidation is underway, with deficits narrowing and government debt remaining moderate.

Despite growth in Armenia's international reserves, balance-of-payments vulnerabilities persist, reflected in wide current account deficits and a large net external liability position.

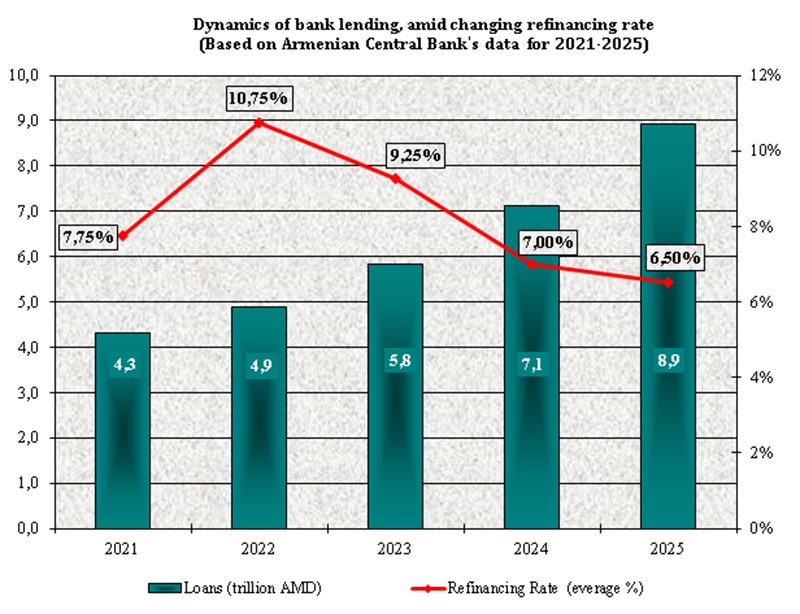

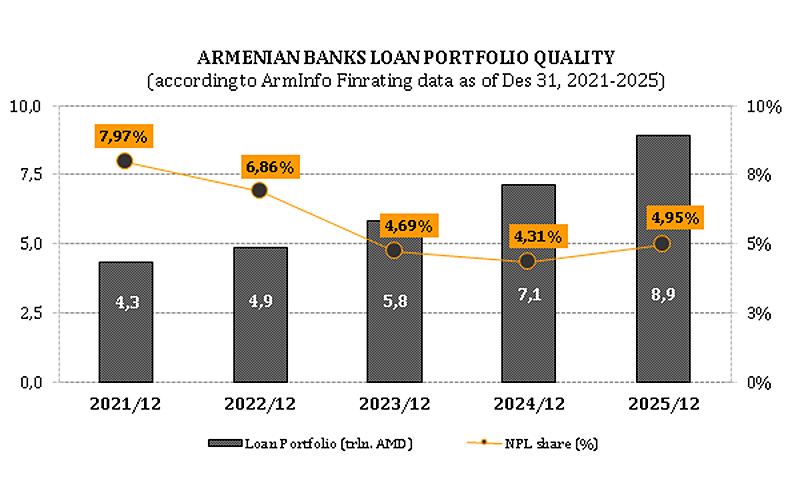

Despite very high loan growth, the banking sector remains stable, underpinned by strong capitalization and high profitability.

Armenia's medium-term fiscal framework reflects a shift toward gradual fiscal consolidation following higher budgetary deficits in 2024-2025. We project the fiscal deficit to average about 3.3% of GDP over 2026-2029. While the 2025 budget targeted a deficit of about 5.5% of GDP, the actual outturn came in at just below 4% of GDP, largely due to the underexecution of planned capital spending. Building on this, the 2026 budget targets a lower deficit of roughly 4.5% of GDP, based on a real economic growth assumption of around 5.5%. Expenditure priorities are rebalanced, with capital investment remaining elevated to support medium-term growth, while defense spending is planned to decline in nominal terms and as a share of GDP, reflecting reduced perceived near-term security pressures following peace negotiations with Azerbaijan. Social spending remains targeted, including continued support for displaced populations and vulnerable households. We forecast the 2026 general government deficit at 4.2% of GDP, below the official target, reflecting our assumption that capital spending will not be executed in full, although this will likely be partly offset by pre-electoral spending pressures. As in recent years, we expect the deficit to be financed primarily through a mix of domestic borrowing and external concessional funding.

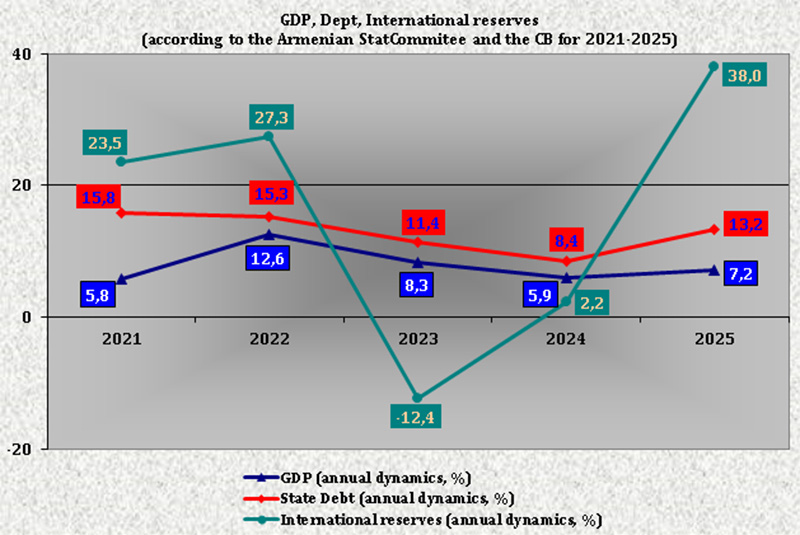

Considering the narrowing fiscal deficits and high nominal GDP growth, we project general government debt, net of liquid assets, to remain broadly stable at a moderate 44% of GDP in the medium term. Fiscal risks from Armenia's housing support program for refugees have diminished relative to our earlier expectations. The program remains restricted to Armenian citizens, which has significantly limited uptake, and its costs are now capped and incorporated into the medium-term fiscal framework, reducing the risk of open-ended liabilities. While faster naturalization (previous Nagorno-Karabakh residents who fled the region becoming Armenian citizens) could raise housing-related spending over time, this risk appears manageable and unlikely to materially alter baseline debt dynamics.

Armenia's balance-of-payments profile remains structurally fragile, characterized by persistent current account deficits, except for the one-off surplus recorded in 2022. As a result, the country maintains a sizable net external liability position, equivalent to roughly 80% of current account receipts, underscoring continued reliance on external financing. As Russia-related inflows (including re-exports) have continued to normalize, the current account balance has weakened, widening to an estimated 6.4% of GDP in 2025 from 4.6% of GDP in 2024.

Looking ahead, we expect the current account deficit to remain elevated at nearly 5% of GDP, on average, annually, as domestic demand remains firm and export growth normalizes. While strong services exports (primarily in tourism) and labor remittances should provide some offset, Armenia's balance-of-payments position is likely to continue to depend on stable access to external financing, including a combination of concessional funding, as well as some private and public commercial borrowing.

Armenia's international reserves strengthened materially in 2025, providing an important buffer amid unpredictable external developments. Gross international reserves rose to a record $5.2 billion in January (18% of GDP), up from about $3.3 billion a year earlier. This increase was driven by a combination of government Eurobond issuance and central bank foreign currency purchases, supported by strong financial and capital inflows from abroad. These reserve buffers should enable the central bank to mitigate risks emanating from potentially volatile capital inflows to the banking system. The banking sector's stock of short-term external debt (primarily nonresident deposits) stands at a relatively large $3.3 billion. We expect reserves to register more modest growth through 2029, rising by around 5% annually.

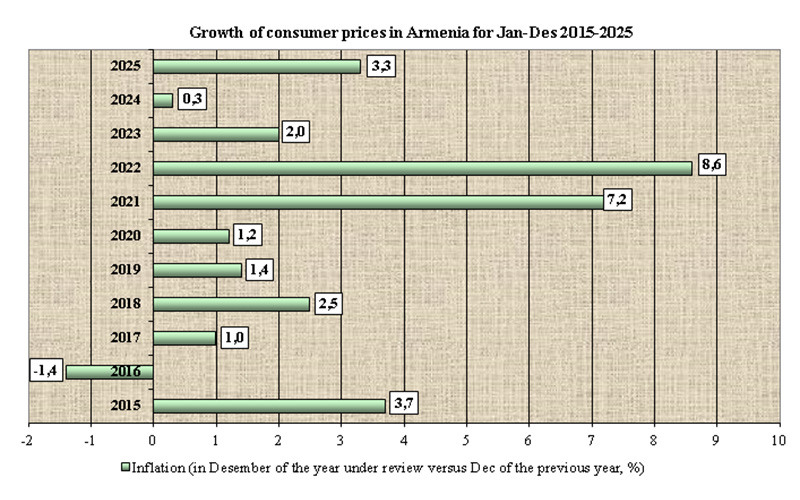

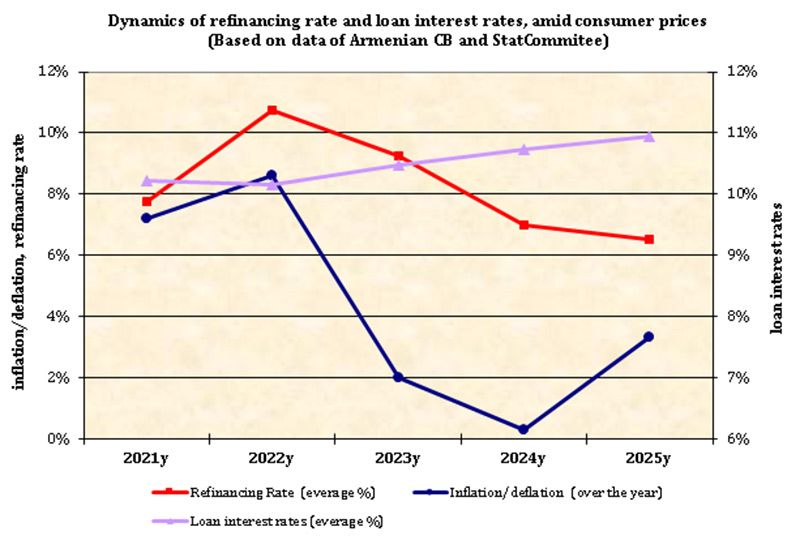

Price pressures have re-emerged after a period of low inflation, with headline inflation rising to 3.8% in January 2026. This compares with 1.7% a year earlier. Accelerating inflation has been driven by higher food prices and increases in transport and education costs. We expect inflation to ease toward an average of around 3.2% in 2026 as economic activity cools. The CBA's strong record of maintaining price stability and its enhanced monetary policy framework enabled it to lower its inflation target to 3% (+/- 1 percentage point) in 2025, from 4% (+/- 1.5 percentage points) previously.

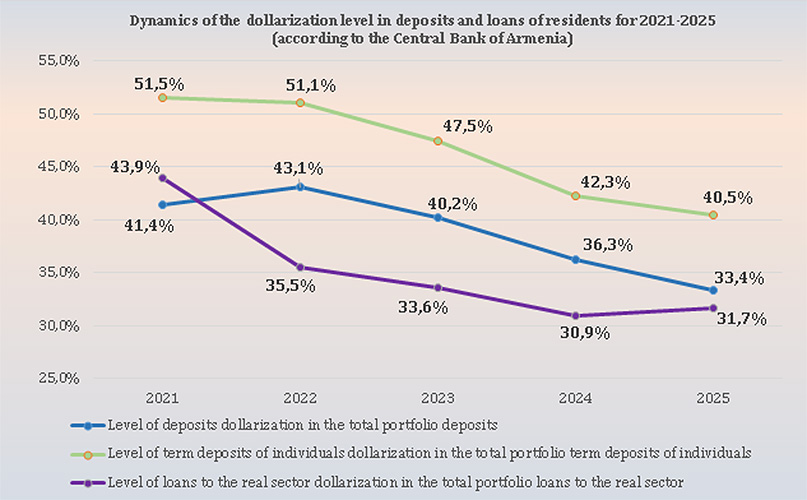

We assess risks to Armenia's financial stability as contained, for now. The banking sector remains well capitalized and highly profitable, supported by strong net interest income, while the rate of credit growth remains above 20% year-on-year, driven mainly by consumer and mortgage lending. The gradual phase-out of mortgage interest tax credits and macroprudential tightening measures have begun to temper housing demand, particularly in Yerevan. Dollarization of banks' assets and liabilities has trended down in recent years with around a third of domestic deposits and loans currently denominated in foreign currency.